Index-Tracking Rigidity and Arbitrage Opportunities in MSCI Index Reconstitutions

“The indexing community has trained customers to think zero tracking error is the goal.”

— Robert D. Arnott (2021), Founder and Chairman of the Board, Research Affiliates

Index-tracking investors tend to rebalance their portfolios with rigidity during index reconstitutions as they are focused on minimising tracking errors. This rigidity generates significant price pressure on the last day before the effective date (hereafter ED-1), creating substantial arbitrage opportunities for market participants. Professor Xin Chang (Nanyang Technological University) and his co-authors—Jiang Luo (Nanyang Technological University), Jiaxin Peng (Capital University of Economics and Business), Shuoge Qian (Singapore University of Social Sciences), and Choon Wee Tan (Advance Capital Partners)—examine the arbitrage opportunities associated with MSCI index reconstitutions across 56 markets worldwide from 2006 to 2023. Their study uncovers the index effects on price and volume patterns, the response of the equity lending market, the presence and impact of index-tracking investors’ rigidity, and the potential arbitrage profits and trading behaviours of arbitrageurs.

Daily and Intraday Index Effects

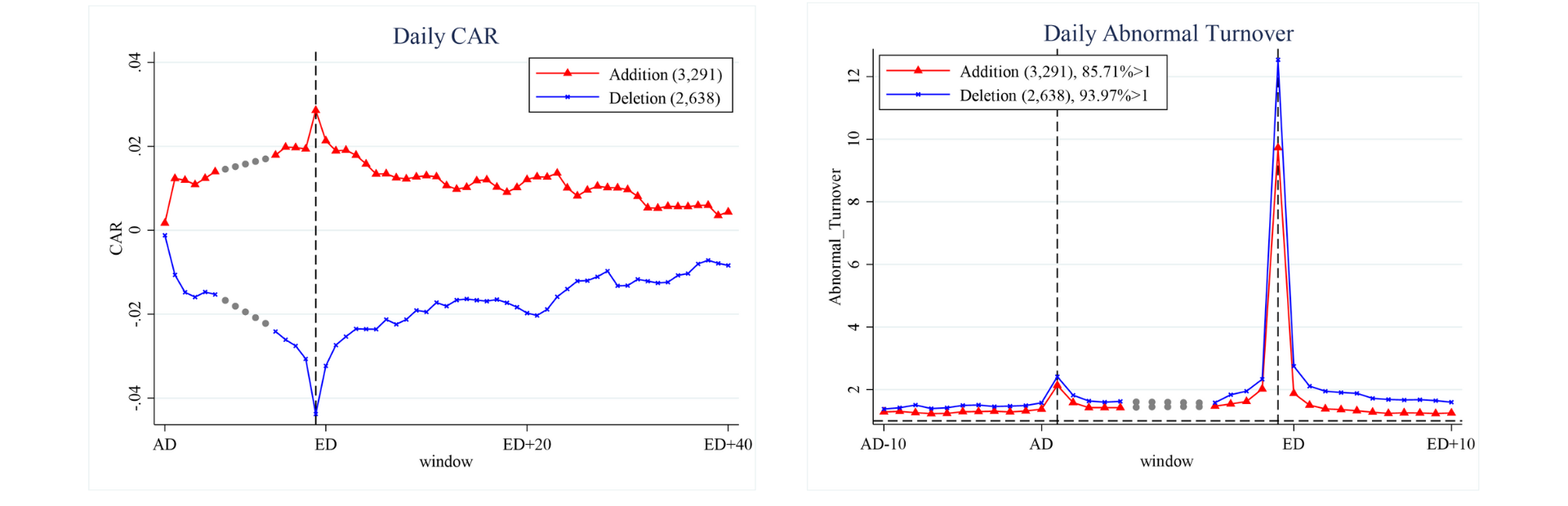

In their research, the daily analysis reveals that the price of added (deleted) stocks begins to rise (decline) on the day after the announcement date (AD+1) and reaches its peak (trough) on ED-1. Exploiting this predictable pattern, arbitrageurs can earn an abnormal return of approximately 5.4% by longing (shorting) added (deleted) stocks at the closing price on AD and closing their positions at the closing price on ED-1, even after accounting for stock lending fees. This strategy generates the highest returns in the Asia-Pacific market at 6.1%, compared to 2.8% in North America. Additionally, trading activity surges significantly on ED-1, with volumes exceeding 10 times the normal levels, underscoring the rigid trading strategies employed by index-tracking investors.

Figure 1: Daily Price

and Volume Pattern

Figure 1: Daily Price

and Volume Pattern

Notably, the intraday analysis reveals that nearly half of this surge occurs in the final minute of the trading session. This suggests that rigid index-tracking investors concentrate their rebalancing on ED-1 and further compress it into the last moments of the day. The intense trading pressure within this short window results in a last-minute return spike of 0.15% for additions and -0.37% for deletions, highlighting the market impact of mechanical index rebalancing. Moreover, the rigidity of index-tracking investors varies across regions. In North America, investors allocate only 23% of their trading volume in the final minute, leading to weaker price pressure on that day. In contrast, European investors concentrate the largest proportion of their trading volume, 71.9%, in the final minute, yet the price impact remains insignificant due to superior market depth. The last-minute price impact is higher in Asia-Pacific and other regions, where trading pressure is more likely to cause significant price impacts. Based on this, this paper also proposes a one-day long-short strategy on ED-1, which yields the highest one-day return in the Asia-Pacific market at 1.2%.

Figure 2: Intraday Price and Volume Pattern

Figure 2: Intraday Price and Volume Pattern

Cross-Sectional Analysis

Their research also finds that the above-documented index effects are significantly related to stock characteristics. Particularly, the abnormal price impact on ED-1 is considerably higher for added stocks with higher pre-event returns, betas, or asset growth, while cumulative price impact during index events is significantly lower for added stocks with higher stock liquidity and profitability. Regarding deletions, both abnormal and cumulative price impact are lower for stocks with lower pre-event returns. For both additions and deletions, trading volume on ED-1 is significantly larger for stocks with higher market values, higher book-to-market ratios, higher leverage, higher stock liquidity, or lower profitability. Arbitrageurs can utilise these findings to implement their strategies. Furthermore, the study finds that over time, index-tracking investors have become less likely to wait until ED-1 to buy added stocks, while arbitrageurs’ short-selling activities for deletions have grown due to the expansion of equity lending markets.

Equity Lending Market’s Response

A significant response from the equity lending market is further observed, substantiating the rigidity of index-tracking investors and the activities of arbitrageurs. First, lending supply rises (falls) sharply shortly after ED for additions (deletions) but remains flat during other periods, suggesting that index-tracking investors, as major suppliers in equity lending markets, purchase (sell) added (deleted) stocks right before the end of ED-1 to minimise tracking errors. Second, short interest in deleted stocks increases steadily before ED-1 and drops sharply afterwards, implying that short-sellers borrow deleted stocks and sell them in the markets while anticipating further stock price decreases before index reconstitutions take effect. Lastly, this paper finds higher stock-borrowing costs and shorter average tenure of equity lending during index reconstitutions, consistent with the short-selling behaviours during index reconstitutions for deleted stocks. These equity lending activities suggest that index-tracking investors prefer to postpone portfolio rebalancing until the end of ED-1, a strategy that arbitrageurs exploit by trading against these predictable patterns.

Index-Tracking Investors, Arbitrageurs and Their Interplay

The study also provides regression evidence on the implications of index-tracking investors’ rigidity and arbitrageurs’ trading activities. First, the analysis shows that past index holdings significantly contribute to the index effects on ED-1, as well as the sharp change in lending supply, highlighting the rigidity of index-tracking investors and their impact on the price pressure of ED-1. Next, the study finds that arbitrageurs’ short-selling activities for deleted stocks depress stock prices before ED-1 but drive them up on ED-1, revealing their trading strategy: borrowing and selling deleted stocks before ED-1 and repurchasing them on ED-1 to close short positions.

Lastly, the rigidity of index-tracking investors is strongly linked to the scale of arbitrageurs’ short-selling activities during the event. This relationship suggests two possible explanations for the interplay between index-tracking investors and arbitrageurs. On one hand, arbitrageurs may engage more aggressively in short selling if they anticipate that index-tracking investors will delay rebalancing until the final moments of ED-1. Conversely, index-tracking investors might deliberately delay rebalancing if they observe elevated short interest before ED-1 and expect short sellers to cover their positions—thus providing liquidity for deleted stocks and helping minimise tracking errors.

In conclusion, this study systematically analyses the index reconstitution across 56 markets, showing that index-tracking investors tend to delay portfolio rebalancing until the final minute before the effective date—a behaviour we term investor rigidity—which amplifies price pressure on ED-1, aligns with notable shifts in the securities lending market and creates significant opportunities for arbitrageurs to exploit and profit.

Note: This research paper is forthcoming in the Pacific-Basin Finance Journal, scheduled for publication in October 2025.

Xin Chang, Simba is a Professor of Finance at Nanyang Business School and Associate Dean (Research), overseeing PhD programs and research activities at Nanyang Business School. He specialises in corporate Finance, especially capital structure, mergers and acquisitions, and stock valuation. He had taught various courses to undergraduate, honours, master, and PhD students at HKUST, the University of Melbourne, the University of Cambridge, and NTU.

Jiang Luo is an Associate Professor of Finance at Nanyang Business School. His earlier academic research was primarily in corporate finance theory. He published several papers on capital budgeting, executive compensation, and entrepreneurship in journals including Journal of Financial Economics, Review of Financial Studies, and Review of Accounting Studies. In recent years, he has been working on understanding the effects of investor psychology on financial markets.

Shuoge Qian is a lecturer of Finance at the School of Business, Singapore University of Social Sciences and a Ph.D. graduate in Banking and Finance at Nanyang Business School. His research interests are Sustainable Finance, Machine Learning and AI, and Behavioral Asset Pricing.

This research paper is a joint work with Jiaxin Peng (Capital University of Economics and Business) and Choon Wee Tan (Advance Capital Partners).